Solayer 101

Learn the basics to advance concepts of staking on Solana & restaking on solayer.

Solayer

Important: Nothing in this article constitutes financial or tax advice. Always consult a tax professional before making any decisions.

Introduction

To liquid stake, or to native stake, that is the question. While this may seem like a simple matter of yield, the truth is that each option has markedly different tax implications.

Firstly, let’s define the two dominant staking models today, both of which are offered by Solayer:

Native staking: where tokens are directly staked to help secure a blockchain network.

Liquid staking (LSTs): where staked assets are represented by tradable tokens, such as sSOL.

In many jurisdictions, including the U.S., native staking and liquid staking are taxed very differently. IRS Revenue Ruling on Staking In 2023 the IRS released their Revenue Ruling 2023-14, which provides explicit guidance on the treatment of staking rewards.

This article outlines the tax consequences of native staking versus liquid staking tokens (LSTs), covering timing and classification of income, risks of double taxation, practical implications for recordkeeping, and institutional considerations. Real-world examples from Solana and Ethereum are used to illustrate the distinctions.

Native Staking: Immediate Taxation, Double-Tax Risk, and Depreciation Exposure

In native staking, investors lock up their crypto directly on-chain or through a validator to earn new units of the same token, like SOL, as rewards. These rewards typically accumulate in the investor’s wallet at regular intervals.

Under Revenue Ruling 2023-14, staking rewards are treated as ordinary income at the moment a taxpayer gains dominion and control over the tokens. Each time new staking rewards hit your wallet, you trigger a taxable event. The value of that reward is based on the fair market value (FMV) at receipt, and must be included in gross income.

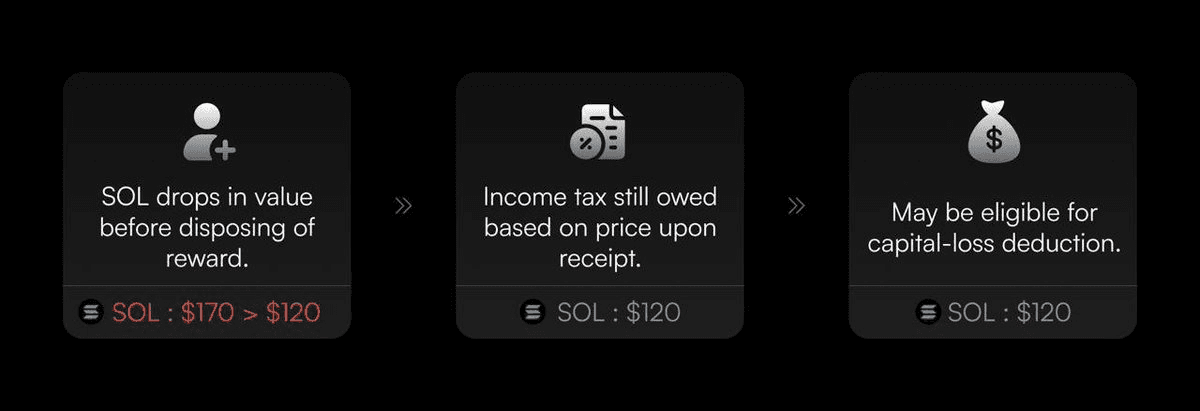

For example, if you receive 1 SOL when SOL is trading at $170, you must report $170 as ordinary income. If you later sell that SOL at a higher price, you must also pay capital-gains tax on the appreciation.

Price-Depreciation Risk

Because the taxable value is fixed at the time of receipt, you remain fully exposed to any subsequent price drop.

Suppose that same SOL you received earlier were to fall from $170 to $120 before you dispose of it, you would still owe income tax on the original $170, even though the reward is now worth only $120. This $50 difference may generate a capital loss when you do eventually sell, but that loss might not fully offset the earlier ordinary-income tax bill.

This is especially true when holding an asset long-term, or where you are subject to capital-loss deduction limits.

In short, native staking can saddle you with an immediate tax liability on a value that can evaporate before you ever fully realise teh gains, compounding the existing double-tax risk.

Liquid Staking: Deferred Taxation and Capital Gains

In liquid staking, you stake tokens through a protocol, like Solayer, and receive a derivative token (e.g. sSOL) that represents your staked position. These tokens can be traded, restaked, used in DeFi, or redeemed later for the underlying asset plus yield.

With LSTs, yield is not paid as new tokens but is reflected in the appreciation of the token’s value or increase in balance (in rebasing designs). Since there’s no new token issued to the investor, there’s generally no income recognized until the LST is sold or redeemed, at which point any gain is treated as a capital gain.

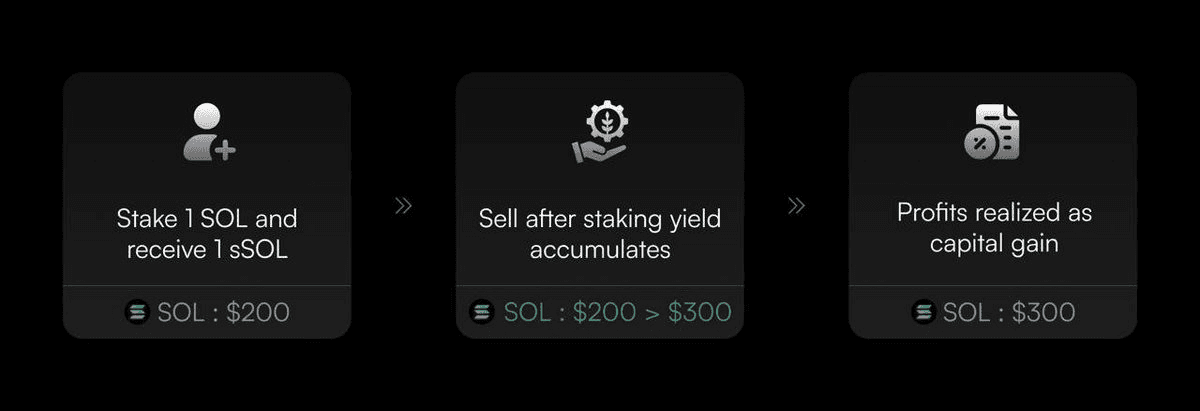

For example, if you stake 1 SOL and receive 1 sSOL valued at $200, and later sell your sSOL for $300 after staking yield accumulates, the $100 gain is realized as a long-term capital gain (if held for more than a year). No tax is triggered during the holding period.

The advantage is clear: LST’s, in most cases, represent a dramatically streamlined and simplified reporting structure.

Other Considerations

Is Swapping into an LST a Taxable Event?

There is some ambiguity as to whether exchanging SOL for sSOL is a taxable event. Under IRS guidance, crypto-for-crypto swaps are generally taxable. However, some argue that receiving an LST is akin to receiving a receipt or claim on your staked asset, and therefore is not a true disposition.

If the swap is done at a 1:1 ratio with no gain or loss, many treat it as non-taxable. Still, most crypto tax software records it as a taxable event. Therefore, it’s best to consult a tax advisor before making any decisions.

Insitiutitonal Preference

Beyond taxes, many institutional investors prefer native staking due to counterparty risk concerns. LSTs rely on smart contracts, which introduce operational risks such as bugs, exploits, or governance failures. For institutions subject to audit, custody regulations, or fiduciary duties, such risks can be unacceptable.

Native staking, while not risk-free, involves direct participation at the protocol level with more predictable, auditable risk. As a result, many institutions prioritize control, security, and compliance over tax efficiency or liquidity, and continue to favor native staking.

Comparative Table: Native Staking vs. LSTs

Conclusion

Both native staking and liquid staking tokens enable investors to earn passive income, but they come with different tax and operational implications.

Native staking results in immediate income tax liability and potential double taxation. LSTs offer tax deferral and lower rates but introduce new risks through reliance on smart contracts.

Retail investors may prefer the tax advantages and flexibility of LSTs. Institutions, on the other hand, often prioritize risk control, transparency, and auditability, making native staking their preferred method.

To access both forms of staking, as well as industry leading yields, visit app.solayer.org.